When It Finally Occurs, Today’s Depression Will Make the Great Depression Look Like a Sunday Picnic

A Tale of Two Depressions

By Reverse Engineer, The Burning PlatformJanuary 6, 2011

JimQ and I have been having a wee bit of a dispute regarding just how much Real Estate values are going to fall as we progress forward with the economic collapse.

Like many Optimistic Pundits here on the net, he holds the belief that if Goobermint support was removed from the RE market and real Price Discovery was allowed, the market would experience perhaps another 20% drop before stabilizing, at which point prudent local savers and international investors would jump back in and buy up the properties in foreclosure.

In Counterpoint to this view, along with a few other Collapse observers like Nicole Foss and Charles Hugh Smith, I consider a much larger drop to be likely, on the order of 80% down from the Peak Mania period prior to the initial 2008 crash. The reason for this is the parallel we are following with the timeline of the Great Depression, beginning actually prior to that with the Mania period of the 1920s.

In this article, I will highlight some of the similarities and differences between your Grandfather’s Depression and this one, and why for the most part I expect it will be an order of magnitude worse in this go round, including the massive collapse of Real Estate values on the order of –80% or more.

Following at the end of this post is a Timeline of significant events and milestones from the period beginning in 1920 through to the 1940s. I will in the course of this article highlight a few of those numbers and events for comparative purposes and show why they are likely to be even worse this time around. Those numbers and events are presented here in [Brackets and Bolded.] For those of you unfamiliar with this Timeline, reviewing it (see the end of this article) prior to reading this post could be worthwhile.

Let’s begin with Real Estate prices which are the driving force in a deflationary depression, and provided the grist for the mill beginning this Point-Counterpoint Debate. The reason for this is that whether the economy is agrarian based or industrial based, during the mania period RE asset prices get inflated by the expanding credit based money in the economy.

In the mostly agrarian economy prior to the 1920s, farmland rose in speculative value as the FSofA provided food for Europe recovering from WWI. However, with Europe mostly recovered by the mid 1920s, the amount of export food dropped and increasing productivity due to mechanization meant less ag land was necessary for food production. As the 1920s progressed, Ag Land lost 30%-40% of its value.

[The value of farmland falls 30 to 40 percent between 1920 and 1929.]

Areas of our country which expanded rapidly with the McMansion Bubble here have experienced a similar decline already, in places like Las Vegas and Florida and California. Nationally, the average decline is less, but a massive inventory of homes are held in shadow inventory which will further depress the market as it becomes necessary to liquidate this inventory.

As the Great Depression progressed onward, the early collapse in RE prices made many Banks insolvent, which then precipitated the Stock Market Crash of 1929. This is an analogue of the sub-prime collapse precipitating the October 2008 collapse of the current market. This creates another feedback loop with RE and commodity prices, and so in Granddad’s Depression by 1932 Farm Prices take a further nosedive losing another 53% in value.

[Farm prices had fallen 53 percent since 1929.]

This reflects the period of the “Grapes of Wrath”, when for all intents and purposes, farmland was basically worthless and many J6P Family farmers lost their farms just for the Taxes owed on them.

We are not at this period yet in Today’s Depression. We are right now rhyming with around 1930, when Da Fed was artificially depressing interest rates and providing liquidity to the market.

[By February 1930, the Federal Reserve has cut the prime interest rate from 6 to 4 percent. Expands the money supply with a major purchase of U.S. securities.]

In the period directly following this (hasn’t happenned yet, but likely will for numerous reasons foreign and domestic), Da Fed finally does pull the liquidity from the market, as then Treasury Secretary Andrew Mellon advocates for Debt Liquidation.

[Treasury Secretary Andrew Mellon announces that the Fed will stand by as the market works itself out: “Liquidate labor, liquidate stocks, liquidate real estate… values will be adjusted, and enterprising people will pick up the wreck from less-competent people.]

As we know now, letting the system fail and liquidating all the malinvestment of that era did not usher in a new era of Prosperity; in fact, things got a whole lot worse after that, and remained so up until massive amounts of new Debt was issued leading into WWII.

We still haven’t even approached the real Crisis Year of 1933 when FDR started making some Socialist Reforms, and the Illuminati of the time attempted to stop the Wealth redistribution with a Military Coup d’Etat.

[Alarmed by Roosevelt’s plan to redistribute wealth from the rich to the poor, a group of millionaire businessmen, led by the Du Pont and J.P. Morgan empires, plans to overthrow Roosevelt with a military coup and install a fascist government. The businessmen try to recruit General Smedley Butler, promising him an army of 500,000, unlimited financial backing and generous media spin control. The plot is foiled when Butler reports it to Congress.]

A good question for Today’s Depression is whether 2-3 years from now, if an attempt like FDRs is made to do a Socialist Wealth redistribution, whether today’s Illuminati will fail in the effort as DuPont and Morgan did, and whether there is somebody with the kind of Integrity General Smedley Butler had to report it, and whether the CONgress Critters would stop such a Coup d’Etat or passively go along with it. If they don’t, our Timeline will diverge at this point and we will pursue a further deepening Fascist paradigm.

Despite the fact we have what already amounts to Depressionary numbers when you look at statistics like the U-6 UE, the increasing number of people on Food Stamps and the massive number of Foreclosures, for the most part unless you are currently living the nightmare, today’s Depression just doesn’t seem quite as bad as Granddad’s Depression, at least not from how you remember it from the Newsreels and Photos of the era.

Even on the international level, the rioting in Greece and the Strikes in France don’t seem to live up to the expectation you have when you look at those old newreels of 1930s era Nazi Rallies. We don’t have the Japanese invading China, we don’t have huge Hoovervilles on the Potomac like the Bonus Army with Vietnam Vets demanding their Bennies.

So how come? Is this Depression just not as bad as the last one? Have we figured out the secret for keeping everything looking good on the surface level while the monetary system disintegrates? Or are we just experiencing the Calm Before the Storm? The answer is both.

First, the worst pictures in your mind of Granddad’s Depression are of gaunt Hobos with the “Brother, Can you Spare a Dime” look on their faces. There are quite a few Bums out there in the Big Shitties these days of course, but at least for the moment the Bum shelter system has been keeping up with the problem. They get swept off the streets on those really cold nights, and though the shelter may be out of beds, they get a place on the floor. During Granddad’s Depression, such a shelter system for those who were on Skid Row wasn’t nearly as developed as it is today.

Even more important is the Hunger problem. In your Granddad’s Depression, the distribution of food to the starving came through Soup Kitchens, so you have the Photos of the lines outside the Kitchen and the sad faces of families sitting around a cafeteria style table eating whatever it was they got served up. Today, we issue SNAP cards which function just like your ATM Card at the checkout, and with the money Da Goobermint drops on the card each month, you can pretty much buy whatever you would like in the grocery store. Exception being anything from the Hot Food counter. I only know this because recently in the checkout line a SNAP card user directly in front of me did not know this, and couldn’t buy the Chinese Buffet special of the day he had scooped up.

In your Granddad’s Depression, you have pictures of the Dustbowl in your head, and the Joad family heading for CA in their rusty old Jalopy on Route 66. Today’s almost nobody lives on Farms on a statistical basis anymore, and if they do they aren’t heading for California. The Jalopies they own are still pretty nice looking cars they bought on Credit, which the Bank isn’t bothering to Repo because then they would have to admit the GMAC Auto Loan had gone south.

Similarly, instead of foreclosing on everybody and pushing them all into Hoovervilles, the McMansions themselves are turning into Hoovervilles. Foreclosures are indefinitely delayed, the residents stop paying the mortgage and squat on the housing until the power and water get turned off, and sometimes even after that. About the only thing that will drive them out now is when they finally run out of money to buy Gas, and become unable to drive to the Walmart 10 miles down the road to buy food with the SNAP card.

That hasn’t happened yet for the most part because in Today’s Depression, UE Bennies have been extended for 2 years. So really at the moment only the very first folks to start taking the hit in 2008 are completely out of Bennies, which will make it interesting to see how it progresses from here with these people. In Europe though, you pretty much can never fall off the UE Dole; there are no expiration dates on the Dole there. In your Granddad’s Depression, though there was some Goobermint Dole, it was very limited.

The existence of most of the social safety nets that have evolved since your Granddad’s depression are the primary reason that so far this one doesn’t LOOK as bad as the old one did in the pictures and the newsreels. Over in Europe, though the population is mighty unhappy over the Austerity measures and gradual evisceration of their Pension system -- current pensioners are still getting their checks; and like here, across the Pond, as of yet, very few people are actually STARVING. That condition is reserved for the truly poor of the world who don’t live in ANY of these countries anymore. In the real 3rd World countries though as the price of a cup of rice or bag of flour goes up here, where there are no SNAP cards -- these folks are on the verge of starvation level conditions, if they are not already there.

In your Granddad’s Depression, as the Jobs disappeared, so also disappeared the Food off the shelves. Farmers couldn’t make a profit on their food as the ability of the people to buy it disappeared. In today’s depression, food keeps moving off the shelves via the SNAP cards, and most Food Production comes not from Family Farms, but from Agribiz, who if they are losing money due to Margin Compression as their Input Prices go up have access to the ZIRP money Helicopter Ben issues out to all TBTF companies. While wholesale prices on the COMEX have recently EXPLODED in upward Volatility, at least my Grocery bill hasn’t changed much. Canned Napa Chili con Carne is still 99 cents a can, even a Ribeye Steak is still coming in at around $7 a pound. That IS around 18% up from as cheap as I could buy it before COMEX prices went up so fast in this cycle, but since food for me only represents about at most 20% of my budget, an increase like this doesn’t affect me much. It can affect very poor people much more of course, but then only if they buy Rib Eye steaks. They can of course substitute cheaper cuts of meat for quite some time, and then start eating Chicken.

Here finally is why at least, to date in most of the 1st World countries, Today’s Depression hasn’t yet seen the kind of social dislocation of your Granddad’s Depression. By this stage of the game in the 1930s, Da Fed had quit on the idea of perpetually pushing new money into the system and Liquidation was Andrew Mellon’s Game. They couldn’t physically even GET money out to all the Failing Banks fast enough in those days to cover the Bank Runs.

Today, to keep enough money in your local Branch Office of your Bank, all Helicopter Ben has to do is click the Free Money function button on his Laptop and direct enough to your bank so when you slide your ATM card through the checkout register and type in your PIN, the Digimoney still appears to be there. A bunch of Regulators may show up on the weekend to “close” your Bank, but by Monday morning its “owned” by a bigger bank in the neighborhood, and Da Goobermint is backstopping all the bad assets on their books. Its still BAU on Monday morning, although a few Branch offices might have closed and a few Tellers are now on the UE line.

As much as you might know that the perpetual money printing game cannot continue in perpetuity, for the time being the additional grease being pushed through the engine has kept the wheels of commerce moving for the last couple of years. Without this Funny Money, Da Goobermint wouldn’t be able to keep the UE Bennies flowing, they wouldn’t be able to keep the money flowing to the Military paying all those soldiers, and keeping people employed in the biznesses that supply the military with all the stuff they need to run a good War. Without the Funny Money, the Social Security checks would stop or at least be seriously cut in size. Worst of all, without the Funny Money, the Bankster Pigmen would not be taking home those Big Bonuses and the parties in the Hamptons would come to a grinding halt.

For anyone who has at least a passing knowledge of history and basic math is concerned watching all this, you know in your Gut that it cannot last in perpetuity. You can’t make Something from Nothing, so you wait for some portion of this vast machine to seize up, and for the ever greater quantities of debt money being issued to simply stop working. For most of us observing this, it already has gone on far longer than I think anyone thought possible. How much longer CAN it go on? Will Jacking Up the Deficit Ceiling by another $2T in March allow the game to be continued onward for another full year? My guess right now is that Yes it Can. Of course, given my track record on short term predictions, this probably means the Sky Will Fall this year. If RE predicts the Sky Will NOT Fall this year, we could be in big trouble. LOL.

In any event, whatever the cause will be of this perpetual motion machine seizing up is, right now it doesn’t look like it will happen first here on these shores. There are many indicators now that the Chinese economy is moving toward a Hyperinflationary endgame, resulting from years of exporting Deflation to the First World countries in the form of depressed labor costs. The systemic problems of the structure of the Euro distributed among states with vastly different economies and political structures are making the instabilities there far greater than they are here, where for the most part our Political system is owned lock stock and barrel by the TBTF Banks.

So the Big Black Swan, when it does inevitably come in for a landing, looks more likely to touch down first in China or Euroland than it does in the FSofA. Not that we will be far behind of course, because then the cascade failure of the Shadow Banking system will begin in earnest.

When it finally does occur of course, then Today’s Depression will make your Granddad’s Depression look like a Sunday Picnic. The various systems developed to maintain order and continuity in the First World countries will seize up. Social Security, SNAP Cards and funding the vast Military will become impossible. Trade will come to a grinding halt, and the lifeblood of our industrial civilization will be unavailable to buy at any price, in any currency, including Gold.

The differences that exist now between your Granddad’s Depression and Today’s Depression are not that great really, and if you go down the list point by point some of the similarities are positively frightening of course. The most important thing to realize here is that in the current timeline, we are only at the very beginning stages, and as Debt Liquidation finally takes hold, all asset classes from Stocks, to Bonds to Real Estate are all destined for massive losses, likely exceeding the 80% loss in the value of Industrial Stocks by 1932.

[Industrial stocks have lost 80 percent of their value since 1930.]

Let me leave you with this final thought. In your Grandfather’s Depression, both Farmland and Industrial Stocks took a MASSIVE hit in asset value. However, in both those cases, they still held SOME intrinsic value. Industry was in its infancy really, and in the 1930s there was plenty of easily accessible Oil right here in the FSofA to grow industry with, once of course more debt was issued to fight WWII. As far as Farmland goes, it always has SOME intrinsic value, even just for Subsistence Farming purposes.

What Intrinsic Value do McMansions have? They are totally dependent on the presence of cheap Oil to run, and themselves are not productive as Farmland. They depend on the ability of the Owner to go out and make a living in some other facet of the economy, and to use his SUV to get there.

As the Jobs disappear and the Oil to run the Cars becomes more scarce and expensive, these White Elephants lose ALL the value they once held. Even if the price on one of them dropped down to 10% of its value, I would not buy one. The model is not sustainable.

Good Ag Land should hold some value here, but even there you have to weigh the Tax Liabilities you will incur with Ownership against what you might be able to sell produce for to an increasingly impoverished general population.

The collapse of Credit in a deflationary depression renders the monetary value of all assets questionable, and just Printing Money does not resolve that problem. It just drives a hyperinflationary spiral for a while before it collapses, but it collapses either way.

The underlying problem here is a collapse of Asset Value that depends on the availability of Cheap Oil. As that disappears, all those assets are rendered WORTHLESS. Not even 20 cents on the Dollar really, that is just an intermediary level here. The model no longer works, because Peak Oil is REAL, and its effects are beginning here. Just BEGINNING friends -- by no means are we yet into the real consequences. We will begin to see them though as the Real Estate market collapses entirely.

Will it happen this year? Probably not. Nevertheless, its Coming Soon to a Theatre Near You.

TIMELINE OF GENERAL EVENTS OF THE GREAT DEPRESSION

1920s (Decade)

* During World War I, federal spending grows three times larger than tax collections. When the government cuts back spending to balance the budget in 1920, a severe recession results. However, the war economy invested heavily in the manufacturing sector, and the next decade will see an explosion of productivity… although only for certain sectors of the economy.

* An average of 600 banks fail each year.

* Agricultural, energy and coal mining sectors are continually depressed. Textiles, shoes, shipbuilding and railroads continually decline.

* The value of farmland falls 30 to 40 percent between 1920 and 1929.

* Organized labor declines throughout the decade. The United Mine Workers Union will see its membership fall from 500,000 in 1920 to 75,000 in 1928. The American Federation of Labor would fall from 5.1 million in 1920 to 3.4 million in 1929.

* “Technological unemployment” enters the nation’s vocabulary; as many as 200,000 workers a year are replaced by automatic or semi-automatic machinery.

* Over the decade, about 1,200 mergers will swallow up more than 6,000 previously independent companies; by 1929, only 200 corporations will control over half of all American industry.

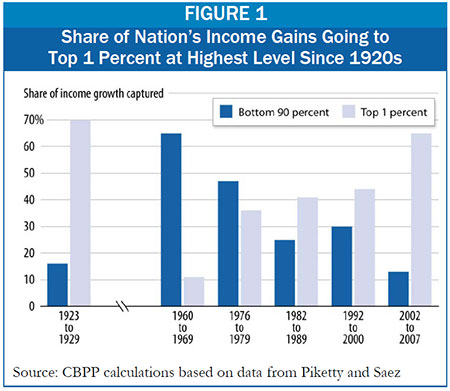

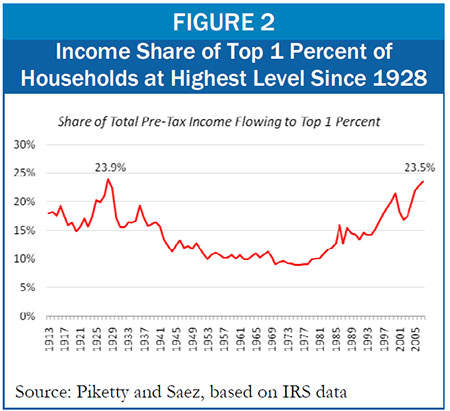

* By the end of the decade, the bottom 80 percent of all income-earners will be removed from the tax rolls completely. Taxes on the rich will fall throughout the decade.

* By 1929, the richest 1 percent will own 40 percent of the nation’s wealth. The bottom 93 percent will have experienced a 4 percent drop in real disposable per-capita income between 1923 and 1929.

* The middle class comprises only 15 to 20 percent of all Americans.

* Individual worker productivity rises an astonishing 43 percent from 1919 to 1929. But the rewards are being funneled to the top: the number of people reporting half-million dollar incomes grows from 156 to 1,489 between 1920 and 1929, a phenomenal rise compared to other decades. But that is still less than 1 percent of all income-earners.

1922

* The conservative Supreme Court strikes down federal child labor legislation.

1923

* President Warren Harding dies in office; his administration was easily one of the most corrupt in American history. Calvin Coolidge, who is squeaky clean by comparison, becomes president. Coolidge is no less committed to laissez-faire and a non-interventionist government. He announces to the American people: “The business of America is business.”

* Supreme Court nullifies minimum wage for women in District of Columbia.

1924

* The Ku Klux Klan reaches the height of its influence in America: by the end of the year it will claim 9 million members. It will decline drastically in 1925, however, after financial and moral scandals rock its leadership.

* The stock market begins its spectacular rise. Bears little relation to the rest of the economy.

1925

* The top tax rate is lowered to 25 percent – the lowest top rate in the eight decades since World War I.

* Supreme Court rules that trade organizations do not violate anti-trust laws as long as some competition survives.

1928

* The construction boom is over.

* Farmers’ share of the national income has dropped from 15 to 9 percent since 1920.

* Between May 1928 and September 1929, the average prices of stocks will rise 40 percent. Trading will mushroom from 2-3 million shares per day to over 5 million. The boom is largely artificial.

1929

* Herbert Hoover becomes President. Hoover is a staunch individualist but not as committed to laissez-faire ideology as Coolidge.

* More than half of all Americans are living below a minimum subsistence level.

* Annual per-capita income is $750; for farm people, it is only $273.

* Backlog of business inventories grows three times larger than the year before. Public consumption markedly down.

* Freight carloads and manufacturing fall.

* Automobile sales decline by a third in the nine months before the crash.

* Construction down $2 billion since 1926.

* Recession begins in August, two months before the stock market crash. During this two month period, production will decline at an annual rate of 20 percent, wholesale prices at 7.5 percent, and personal income at 5 percent.

* Stock market crash begins October 24. Investors call October 29 “Black Tuesday.” Losses for the month will total $16 billion, an astronomical sum in those days.

* Congress passes Agricultural Marketing Act to support farmers until they can get back on their feet.

1930

* By February, the Federal Reserve has cut the prime interest rate from 6 to 4 percent. Expands the money supply with a major purchase of U.S. securities. However, for the next year and a half, the Fed will add very little money to the shrinking economy. (At no time will it actually pull money out of the system.) Treasury Secretary Andrew Mellon announces that the Fed will stand by as the market works itself out: “Liquidate labor, liquidate stocks, liquidate real estate… values will be adjusted, and enterprising people will pick up the wreck from less-competent people.” (More)

* The Smoot-Hawley Tariff passes on June 17. With imports forming only 6 percent of the GNP, the 40 percent tariffs work out to an effective tax of only 2.4 percent per citizen. Even this is compensated for by the fact that American businesses are no longer investing in Europe, but keeping their money stateside. The consensus of modern economists is that the tariff made only a minor contribution to the Great Depression in the U.S., but a major one in Europe. (More)

* The first bank panic occurs later this year; a public run on banks results in a wave of bankruptcies. Bank failures and deposit losses are responsible for the contracting money supply.

* Supreme Court rules that the monopoly U.S. Steel does not violate anti-trust laws as long as competition exists, no matter how negligible.

* Democrats gain in Congressional elections, but still do not have a majority.

* The GNP falls 9.4 percent from the year before. The unemployment rate climbs from 3.2 to 8.7 percent.

1931

* No major legislation is passed addressing the Depression.

* A second banking panic occurs in the spring.

* The GNP falls another 8.5 percent; unemployment rises to 15.9 percent.

1932

* This and the next year are the worst years of the Great Depression. For 1932, GNP falls a record 13.4 percent; unemployment rises to 23.6 percent.

* Industrial stocks have lost 80 percent of their value since 1930.

* 10,000 banks have failed since 1929, or 40 percent of the 1929 total.

* About $2 billion in deposits have been lost since 1929.

* Money supply has contracted 31 percent since 1929.

* GNP has also fallen 31 percent since 1929.

* Over 13 million Americans have lost their jobs since 1929.

* Capital growth investments have dropped from $16.2 billion to 1/3 of one billion since 1929.

* Farm prices have fallen 53 percent since 1929.

* International trade has fallen by two-thirds since 1929.

* The Fed makes its first major expansion of the money supply since February 1930.

* Congress creates the Reconstruction Finance Corporation. (More)

* Congress passes the Federal Home Loan Bank Act and the Glass-Steagall Act of 1932. (More)

* Top tax rate is raised from 25 to 63 percent.

* Popular opinion considers Hoover’s measures too little too late. Franklin Roosevelt easily defeats Hoover in the fall election. Democrats win control of Congress.

* At his Democratic presidential nomination, Roosevelt says: “I pledge you, I pledge myself, to a new deal for the American people.”

1933

* Roosevelt inaugurated; begins “First 100 Days” of intensive legislative activity. (More)

* A third banking panic occurs in March. Roosevelt declares a Bank Holiday; closes financial institutions to stop a run on banks.

* Alarmed by Roosevelt’s plan to redistribute wealth from the rich to the poor, a group of millionaire businessmen, led by the Du Pont and J.P. Morgan empires, plans to overthrow Roosevelt with a military coup and install a fascist government. The businessmen try to recruit General Smedley Butler, promising him an army of 500,000, unlimited financial backing and generous media spin control. The plot is foiled when Butler reports it to Congress. (More)

* Congress authorizes creation of the Agricultural Adjustment Administration, the Civilian Conservation Corps, the Farm Credit Administration, the Federal Deposit Insurance Corporation, the Federal Emergency Relief Administration, the National Recovery Administration, the Public Works Administration and the Tennessee Valley Authority. (More)

* Congress passes the Emergency Banking Bill, the Glass-Steagall Act of 1933, the Farm Credit Act, the National Industrial Recovery Act and the Truth-in-Securities Act. (More)

* U.S. goes off the gold standard.

* Roosevelt does much to redistribute wealth from the rich to the poor, but is obsessed with a balanced budget. He later rejects Keynes’ advice to begin heavy deficit spending.

* The free fall of the GNP is significantly slowed; it dips only 2.1 percent this year. Unemployment rises slightly, to 24.9 percent.

1934

* Congress authorizes creation of the Federal Communications Commission, the National Mediation Board and the Securities and Exchange Commission. (More)

* Congress passes the Securities and Exchange Act and the Trade Agreement Act. (More)

* The economy turns around: GNP rises 7.7 percent, and unemployment falls to 21.7 percent. A long road to recovery begins.

* Sweden becomes the first nation to recover fully from the Great Depression. It has followed a policy of Keynesian deficit spending. (More)

1935

* The Supreme Court declares the National Recovery Administration to be unconstitutional.

* Congress authorizes creation of the Works Progress Administration, the National Labor Relations Board and the Rural Electrification Administration. (More)

* Congress passes the Banking Act of 1935, the Emergency Relief Appropriation Act, the National Labor Relations Act, and the Social Security Act. (More)

* Economic recovery continues: the GNP grows another 8.1 percent, and unemployment falls to 20.1 percent.

1936

* The Supreme Court declares part of the Agricultural Adjustment Act to be unconstitutional.

* In response, Congress passes the Soil Conservation and Domestic Allotment Act. (More)

* Top tax rate raised to 79 percent.

* Economic recovery continues: GNP grows a record 14.1 percent; unemployment falls to 16.9 percent.

* Germany becomes the second nation to recover fully from the Great Depression, through heavy deficit spending in preparation for war.

1937

* The Supreme Court declares the National Labor Relations Board to be unconstitutional.

* Roosevelt seeks to enlarge and therefore liberalize the Supreme Court. This attempt not only fails, but outrages the public.

* Economists attribute economic growth so far to heavy government spending that is somewhat deficit. Roosevelt, however, fears an unbalanced budget and cuts spending for 1937. That summer, the nation plunges into another recession. Despite this, the yearly GNP rises 5.0 percent, and unemployment falls to 14.3 percent.

1938

* Congress passes the Agricultural Adjustment Act of 1938 and the Fair Labor Standards Act. (More)

* No major New Deal legislation is passed after this date, due to Roosevelt’s weakened political power.

* The year-long recession makes itself felt: the GNP falls 4.5 percent, and unemployment rises to 19.0 percent.

* Britain becomes the third nation to recover as it begins deficit spending in preparation for war.

1939

* GNP rises 7.9 percent; unemployment falls to 17.2 percent.

* The United States will begin emerging from the Depression as it borrows and spends $1 billion to build its armed forces. From 1939 to 1941, when the Japanese attack Pearl Harbor, U.S. manufacturing will have shot up a phenomenal 50 percent!

* The Depression is ending worldwide as nations prepare for the coming hostilities.

* World War II starts with Hitler’s invasion of Poland.

1945

* Although the war is the largest tragedy in human history, the United States emerges as the world’s only economic superpower. Deficit spending has resulted in a national debt 123 percent the size of the GDP. By contrast, in 1994, the $4.7 trillion national debt will be only 70 percent of the GDP!

* The top tax rate is 91 percent. It will stay at least 88 percent until 1963, when it is lowered to 70 percent. During this time, America will experience the greatest economic boom it has ever known.

The Great Depression: The Business Plot to Overthrow Roosevelt

By Steve Kangas, The Great Depression: Its Causes and CureCopyright 1996

In the summer of 1933, shortly after Roosevelt's "First 100 Days," America's richest businessmen were in a panic. It was clear that Roosevelt intended to conduct a massive redistribution of wealth from the rich to the poor. Roosevelt had to be stopped at all costs.

The answer was a military coup. It was to be secretly financed and organized by leading officers of the Morgan and Du Pont empires. This included some of America's richest and most famous names of the time:

- Irenee Du Pont - Right-wing chemical industrialist and founder of the American Liberty League, the organization assigned to execute the plot.

- Grayson Murphy - Director of Goodyear, Bethlehem Steel and a group of J.P. Morgan banks.

- William Doyle - Former state commander of the American Legion and a central plotter of the coup.

- John Davis - Former Democratic presidential candidate and a senior attorney for J.P. Morgan.

- Al Smith - Roosevelt's bitter political foe from New York. Smith was a former governor of New York and a codirector of the American Liberty League.

- John J. Raskob - A high-ranking Du Pont officer and a former chairman of the Democratic Party. In later decades, Raskob would become a "Knight of Malta," a Roman Catholic Religious Order with a high percentage of CIA spies, including CIA Directors William Casey, William Colby and John McCone.

- Robert Clark - One of Wall Street's richest bankers and stockbrokers.

- Gerald MacGuire - Bond salesman for Clark, and a former commander of the Connecticut American Legion. MacGuire was the key recruiter to General Butler.

What the businessmen proposed was dramatic: they wanted General Butler to deliver an ultimatum to Roosevelt. Roosevelt would pretend to become sick and incapacitated from his polio, and allow a newly created cabinet officer, a "Secretary of General Affairs," to run things in his stead. The secretary, of course, would be carrying out the orders of Wall Street. If Roosevelt refused, then General Butler would force him out with an army of 500,000 war veterans from the American Legion. But MacGuire assured Butler the cover story would work:

- "You know the American people will swallow that. We have got the newspapers. We will start a campaign that the President's health is failing. Everyone can tell that by looking at him, and the dumb American people will fall for it in a second…"

And what type of government would replace Roosevelt's New Deal? MacGuire was perfectly candid to Paul French, a reporter friend of General Butler's:

- "We need a fascist government in this country… to save the nation from the communists who want to tear it down and wreck all that we have built in America. The only men who have the patriotism to do it are the soldiers, and Smedley Butler is the ideal leader. He could organize a million men overnight."

If this sounds too fantastic to believe, we should remember that by 1933, the crimes of fascism were still mostly in the future, and its dangers were largely unknown, even to its supporters. But in the early days, many businessmen openly admired Mussolini because he had used a strong hand to deal with labor unions, put out social unrest, and get the economy working again, if only at the point of a gun. Americans today would be appalled to learn of the many famous millionaires back then who initially admired Hitler and Mussolini: Henry Ford, John D. Rockefeller, John and Allen Dulles (who, besides being millionaires, would later become Eisenhower's Secretary of State and CIA Director, respectively), and, of course, everyone on the above list. They disavowed Hitler and Mussolini only after their atrocities grew to indefensible levels.

The plot fell apart when Butler went public. The general revealed the details of the coup before the McCormack-Dickstein Committee, which would later become the notorious House Un-American Activities Committee. (In the 50s, this committee would destroy the lives of hundreds of innocent Americans with its communist witch hunts.)

The Committee heard the testimony of Butler and French, but failed to call in any of the coup plotters for questioning, other than MacGuire. In fact, the Committee whitewashed the public version of its final report, deleting the names of powerful businessmen whose reputations they sought to protect. The most likely reason for this response is that Wall Street had undue influence in Congress also.

Even more alarming, the elite-controlled media failed to pick up on the story, and even today the incident remains little known. The elite managed to spin the story as nothing more than the rumors and hearsay of Butler and French, even though Butler was a Quaker of unimpeachable honesty and integrity. Butler, appalled by the cover-up, went on national radio to denounce it, but with little success.

Butler was not vindicated until 1967, when journalist John Spivak uncovered the Committee's internal, secret report. It clearly confirmed Butler's story:

- In the last few weeks of the committee's life it received evidence showing that certain persons had attempted to establish a fascist organization in this country…

There is no question that these attempts were discussed, were planned and might have been placed in execution if the financial backers deemed it expedient…

MacGuire denied [Butler's] allegations under oath, but your committee was able to verify all the pertinent statements made to General Butler, with the exception of the direct statement suggesting the creation of the organization. This, however, was corroborated in the correspondence of MacGuire with his principle, Robert Sterling Clark, of New York City, while MacGuire was abroad studying the various form of veterans' organizations of Fascist character.

Exposed: How the U.S. Government Is Hiding the Depression

Financial SenseDecember 29, 2010

The real US unemployment rate is not 9.8% but between 25% and 30%. That is a depression level of job losses -- so why doesn't it look like a depression for many people? How can so large of a statistical discrepancy exist, and how is it that holiday shopping malls are so crowded in a depression?

The true devastation is hidden by essentially placing the job losses inside three different "boxes": the official unemployment box, the true full unemployment box, and most importantly, the staggering and persistent private sector job loss box that has been temporarily covered over by a fantastic level of governmental deficit spending. The "recovering and out of the recession" cover story is only plausible when nobody connects the dots and adds all the boxes together.

We will add together the three boxes herein -- using US government statistics for all three -- and convincingly show that the US economy is in far worse condition than what is presented by the government or by the mainstream media. No, we have not emerged from "recession" and there will be no "double dip" -- because the first "dip" was straight down to a depression-level economy in 2008/2009, and we haven't come back up.

Creating artificial "free money" on a massive scale that artificially boosts short-term employment is how you segment depression level unemployment into the separate boxes and hide what is really happening. It is this radical strategy that most distinguishes the current downturn from the 1970s and 1930s. The ultimate source of most of the current "free money" that hides the depression is the government risking the impoverishment of US savers and investors for potentially decades to come, with the worst of the damage concentrated on retirees and Boomers.

To have a chance of defending your hoped-for future lifestyle, there is simply no substitute for seeing the truth clearly. For it is only when we see through the lies with clarity that we can distinguish the false opportunity of manipulated markets from the real opportunities that can be found in unexpected places.

Headline Unemployment (Box 1)

The graph above is our starting point and first "box". It is the "headline" rate of unemployment in the US that is featured in newspaper articles and discussed on the cable business news. As of November 2010 the official US unemployment rate was 9.8%. While that's deeply painful, and unemployment rates since 2008 have been the highest seen since the end of the Great Depression (with the exception of the 10.8% peak in 1982), 9.8% is not a depression level unemployment rate.

Real Unemployment (Box 2)

As economists and political decision makers know quite well, the "official" unemployment rate is not the full rate of US unemployment. The "official" rate is technically known as the U3 rate of unemployment, and it is a politically advantageous partial accounting for the unemployed. The U.S. Bureau of Labor Statistics calculates unemployment 6 different ways, U1-U6, and it is only in the U6 statistic that all the categories of unemployment are added together.The two biggest differences between the U3 official rate of unemployment and the U6 full rate of unemployment are in the treatment of the long-term unemployed and involuntary part-time workers. If you've been out of work for a long time, you badly want a job, but you know from your long search that nobody in your area is hiring; you already have applications on file at every reasonable prospect, and you haven't filled out a new application recently -- then from an official perspective (U3), you are not only no longer unemployed, you just became a non-person altogether. Alternatively, if you have a master's degree in engineering, lost your job, and are working 15 hours a week (the most you can get) in a convenience store at minimum wage to keep a little money coming in, then from an official (U3) perspective you would be fully employed. In contrast, U6 is the most inclusive measure of unemployment, as it includes both the long-term unemployed and the involuntary part-time categories. Thus, individuals in each of the situations described above would be included in the U6 measure.

The green bar segment in the graph above illustrates what happens when we look at the full, U6 measure of unemployment as reported by the U.S. Bureau of Labor Statistics for November of 2010. Our unemployment rate almost doubles, as we go from 9.8% to 17% of the civilian work force being unemployed. The real unemployed go from one in ten workers, to one in six workers. The difference between a just-under-10% unemployment rate and a close to 20% rate of unemployment is the difference between recession and depression.

Unfortunately, there is more in the mix than simple unemployment statistics, and when we look inside the "third box" in the next section, we will see that the economic situation is not a mild depression, but rather a full blown major depression.

To try to prevent a flood of corrective e-mails from readers, let me state that the challenge I set for myself in writing this article was to illustrate what was happening using only official US government numbers. Meaning, in my opinion, using unreliable and deliberately misleading numbers that have been subjected to increasing degrees of political manipulation over the decades. I have been writing articles for years that have discussed increasing government manipulation of inflation statistics, and am well aware of the work of John Williams and others in trying to independently determine genuine inflation and unemployment rates. I personally believe that the real inflation and unemployment rates are substantively higher that what is being reported to us, and that the real U6 measure is likely 20% or above.

That said, I wanted to separate the concept of the three boxes from the concepts of statistical manipulation, so there were no distractions for a reader who was skeptical about manipulations, i.e. whether the US government would abuse the fine print of economic statistics to mislead its citizens for political purposes. If you have no trouble accepting that the government manipulates statistics for political advantage, then understand that the situation is significantly worse than what is illustrated herein.

The Gaping Hole In The Economy

To see what a real depression looks like, take a long look at the graph below, which shows what happened to the US economy between 2007 and 2009. As shown with the blue bars and the chart below the graph, the size of the US private sector economy plunged by $1.3 trillion -- and it hasn't come back.

Yet, we don't see the full extent of this plunge around us on the streets or in the headlines. Indeed, despite this ongoing, gaping hole in the US economy, the official story is that the US isn't even in a recession. What happened to all of the job losses from this rapid and persistent collapse of a large section of the US private economy?

The answers can be found in the red and yellow bars above, representing Federal government spending and state and local government spending. Federal spending rose by $700 billion, and state and local government spending rose by $300 billion. (With the state and local spending being funded by Federal government transfers that have been netted out, so it is really almost all growth in Federal spending.) The private economy plummeted by $1.3 trillion while the government economy soared by $1 trillion, and we were left with what looks like a much more manageable $300 billion shrinkage, the kind of economic change that might be associated with a 9.8% official unemployment rate. In other word, a little over 75% of the collapse in the private economy was (and is) being covered by increased government spending.